A few years ago, I shared a simple yet powerful idea for managing your portfolio in retirement: hold a low-cost, globally diversified equity ETF for long-term growth, and pair it with a high-interest savings ETF or money market fund to cover short-term cash flow needs (12-24 months).

I called it a two-fund solution, and the core idea was to eliminate complexity while reducing the behavioural risks that trip up so many retirees – things like selling during market downturns, holding too much cash out of fear, or managing a complicated mess of stocks and funds.

More recently, after digging into research from Scott Cederburg and others, it’s become clear that a globally diversified all-equity strategy may be optimal for investors to hold throughout their lifetime.

That’s why a fund like VEQT (with its roughly 30% domestic, 70% international mix) may be ideal for self-directed investors to hold both during their working years AND throughout retirement.

Related: VEQT and Chill for Life?

Indeed, VEQT’s structure not only simplifies investing for self-directed investors but also aligns with cutting-edge research on optimal lifetime asset allocation.

In this updated article, we’re blending the academic research with behavioural practicality. The Two-Fund Retirement Solution gives you long-term growth, short-term stability, and (in theory) a higher chance of staying invested when it matters most.

The Problem: Selling When Markets Are Down

Even the most diversified, evidence-based portfolios like VEQT are still 100% equities. That’s great for long-term growth. But it also means they’ll experience steep drawdowns from time to time.

For retirees who rely on portfolio withdrawals, that’s a real problem. It’s incredibly hard – psychologically – to sell shares when they’re down 20% or more. You know you’re supposed to stay the course, but when your income depends on those shares, logic takes a backseat. This triggers:

-

Loss aversion (“I’m locking in a loss!”)

-

Market timing impulses (“Maybe I’ll wait until it comes back up…”)

-

Cash flow stress if income needs are inflexible

This is how people start with an equity portfolio and end up in GICs.

The Solution: Pair Growth with Liquidity

The Two-Fund Retirement Solution solves for this by carving out a small portion of your portfolio – 10% or so – and parking it in a high-interest savings ETF or money market fund (like CASH.TO, CSAV, or PSA).

| Holding | Allocation |

| VEQT (or similar) | 90% |

| HISA ETF | 10% |

How To Use It

- Withdrawals come from the HISA fund, not your VEQT holdings.

- Turn off automatic dividend reinvestment (DRIP) on VEQT. Let those dividends flow into cash instead – this helps refill the HISA sleeve passively over time.

- Refill the HISA bucket during up markets (or on a regular annual schedule).

- Keep roughly 12 months of planned withdrawals in the HISA fund to weather market storms.

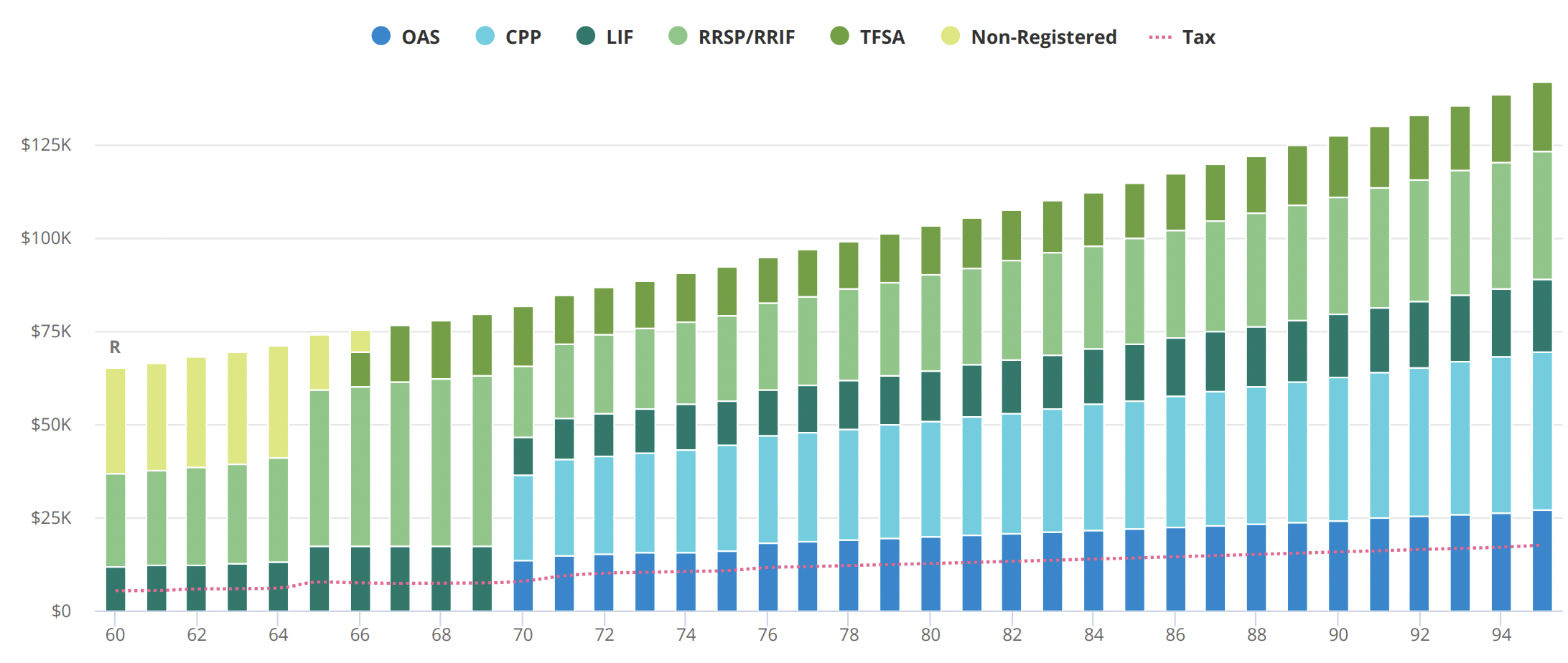

Case Study: Two-Fund Retirement Solution in Action

Meet Sarah, a 60-year-old single retiree who retired at the end of 2024. She has the following assets:

- $500,000 in an RRSP

- $240,000 in a LIRA

- $150,000 in a TFSA

- $100,000 in a non-registered investment account

- $50,000 in a high-interest savings account

Her goal: Spend $60,000 per year after tax and defer CPP and OAS until age 70 to maximize guaranteed income.

The Two-Fund Strategy in Action

Sarah invests 90% of her RRSP, LIRA, and non-registered portfolio in VEQT, taking advantage of its global equity exposure and low cost. She keeps the remaining 10% in a high-interest savings ETF, which she uses for withdrawals in the early years. Her TFSA remains in 100% VEQT until age 65 – it’s the account she’ll touch last, once the non-registered funds are exhausted.

- She turns off dividend reinvestment on VEQT, allowing dividends to accumulate in cash.

- From age 60 to 69, she draws primarily from her RRSP and LIRA, gradually reducing her tax-deferred balances.

- Her TFSA is untouched during this phase, growing tax-free and serving as a long-term reserve or legacy asset.

What the Projections Show

Using realistic return and inflation assumptions (5.6% after-tax return, 2.1% inflation), Sarah’s plan is well within reach:

- Her withdrawal strategy maintains a 105% funded status

- Her portfolio lasts to age 95, even with conservative assumptions

- By delaying CPP and OAS to age 70, she increases her benefits by 42% and 36% respectively, versus taking the benefits at 65.

Final Thoughts

I tell my clients they should aim to take as much equity risk as they’re willing to stomach in retirement. For some, that’s 50-60% equities, for others that’s up to 100% equities.

Meanwhile, good recent research says the optimal portfolio to hold throughout your lifetime is 1/3 domestic equities and 2/3 international equities.

The problem is that research was done with numbers on a spreadsheet – and while the numbers recovered after steep losses from major market crashes, a spreadsheet is not reflective of how a real-life retiree would feel about their portfolio and staying the course.

In other words, it’s easier to look backwards and see that everything worked out, but it’s much more difficult staring at actual losses in your portfolio without a crystal ball to show you the path forward.

That’s why, while “sub-optimal”, I suggest investors pair their risk appropriate asset allocation ETF with a 10% cash wedge (HISA ETF) to help facilitate withdrawals in retirement. What you give up in expected returns by holding some cash, you gain in peace of mind and psychological benefits to combat heuristics like loss aversion.

Have any retirees put the Two-Fund Retirement Solution into action? Let us know in the comments.

Leave a Reply