One reason why retirement planning is so challenging to think about is because we often go from receiving one income stream (our T4 salary income) to juggling several different income streams throughout retirement.

Even more confusing is the fact that those retirement income streams often can (or should) arrive at different times and may have different tax treatments.

Why do you need a retirement plan?

Consider that you might draw an income from the following sources in retirement:

- Defined benefit pension

- RRSP or RRIF

- LIF

- TFSA

- Non-registered investments

- Non-registered savings

- Corporation

- CPP

- OAS

Let’s explore a potentially dizzying array of decisions.

Members of a defined benefit pension plan will have to make a tricky decision about when to retire (early and reduced, earliest unreduced, or normal retirement date). Then they’ll need to select from a menu of joint and survivor options (100%, 67%, 60%, 50%) with or without a 5, 10, or 15 year guarantee if you die early.

Those with a spouse are required to choose a joint life pension option that leaves their spouse a percentage of the monthly pension payments if they die first, however your spouse can sign a waiver giving up their rights to this benefit.

You can withdraw from an RRSP at any age before it must collapse at the end of the year you turn 71.

A RRIF conversion must be done at that time, but it can happen earlier and might make the most sense at 65 when RRIF income becomes eligible pension income and can be split with a spouse or common law partner.

A LIRA to LIF conversion has to wait until at least age 55 in most cases, and similarly must be done by the end of the year you turn 71. This conversion can also come with another decision around unlocking 50% to 100% of the LIF (depending on the jurisdiction) to move into a more flexible RRSP or RRIF.

TFSA withdrawals can be done at any time and for any reason, and withdrawals are completely tax free. The added bonus is that you get the contribution room back the following year after a withdrawal is made. But it might be wise to leave your TFSA funds intact to act as a margin of safety or tax-free pot of money for your beneficiaries.

Small business owners have the added complexity of winding-down their corporation by withdrawing funds personally via dividends.

Those with non-registered investments need to consider capital gains from the sale of stocks or funds that have appreciated in value over the years. Capital gains are taxed favourably, since only 50% (half) of the gain is considered taxable and added to your income (but only when sold). Investment income earned from dividends and interest are taxable in the year received.

Non-registered savings from a regular savings account is money that you have already paid tax on earlier, although as explained above the interest income earned is fully taxable in the year received.

Then there are your government benefits (CPP and OAS) to consider.

You can take your CPP as early as age 60, but it’s often a mistake to do so because of the permanent 36% early take-up penalty. Taking CPP at 65 would be considered your normal retirement age with no penalty. And those who can wait to take their CPP at 70 will see their benefits rise by 42% (plus inflation adjustments).

OAS, meanwhile, cannot be claimed earlier than 65 but will automatically start at that age unless you tell Service Canada otherwise. As long as you’ve lived in Canada for 40 years between 18 and 65 you’ll get 100% of your entitled OAS benefits (before clawback considerations). Subtract 2.5% for every year that you were not in Canada during that time. Delaying OAS to age 70 will lead to 36% more in benefits (plus inflation adjustments).

Putting the Puzzle Pieces Together

In my advice-only financial planning practice I explain to clients that I’m trying to help them fit their retirement income puzzle pieces together in the most tax efficient way to meet their retirement spending needs.

I liken it to trying to get your car out of the parking garage in one of those 3D puzzle games.

Some puzzle pieces need to be moved aside to make room for other income streams to come online.

For instance, it’s now widely accepted that most Canadians are going to get more lifetime income if they delay taking CPP until 70. But I don’t want you to delay living your best early retirement lifestyle until 70 when your benefits kick-in. We’re just going to get the income from somewhere else, like your RRSP or RRIF with perhaps a top-up from non-registered funds.

The result from shifting these puzzle pieces around is that you maximize your lifetime spending and minimize your lifetime taxes.

Indeed, we can fool ourselves into keeping our tax rate extremely low in our 60s by drawing from our non-registered savings and TFSA, only to discover we’ve kicked a major tax problem down the road when the inevitable collision of taxable income from our RRIF, CPP, and OAS begins in our 70s.

Our Retirement Income Plan

My wife and I have more complicated finances than most regular T4 salaried employees because we’re incorporated and have built up significant assets inside our corporation that will need to be withdrawn in retirement.

So we need to be extra careful designing our retirement income to meet our desired lifestyle spending while also keeping tax efficiency in mind.

This takes a delicate approach that is highly influenced by our retirement date, or when we stop earning an income.

Work too long, and the window shrinks to get funds out of the corporation before CPP and OAS and ever-increasing RRIF and LIF minimum withdrawal requirements kick-in.

Retire too early (and spend too much) and you risk exhausting your resources before CPP and OAS come to the rescue.

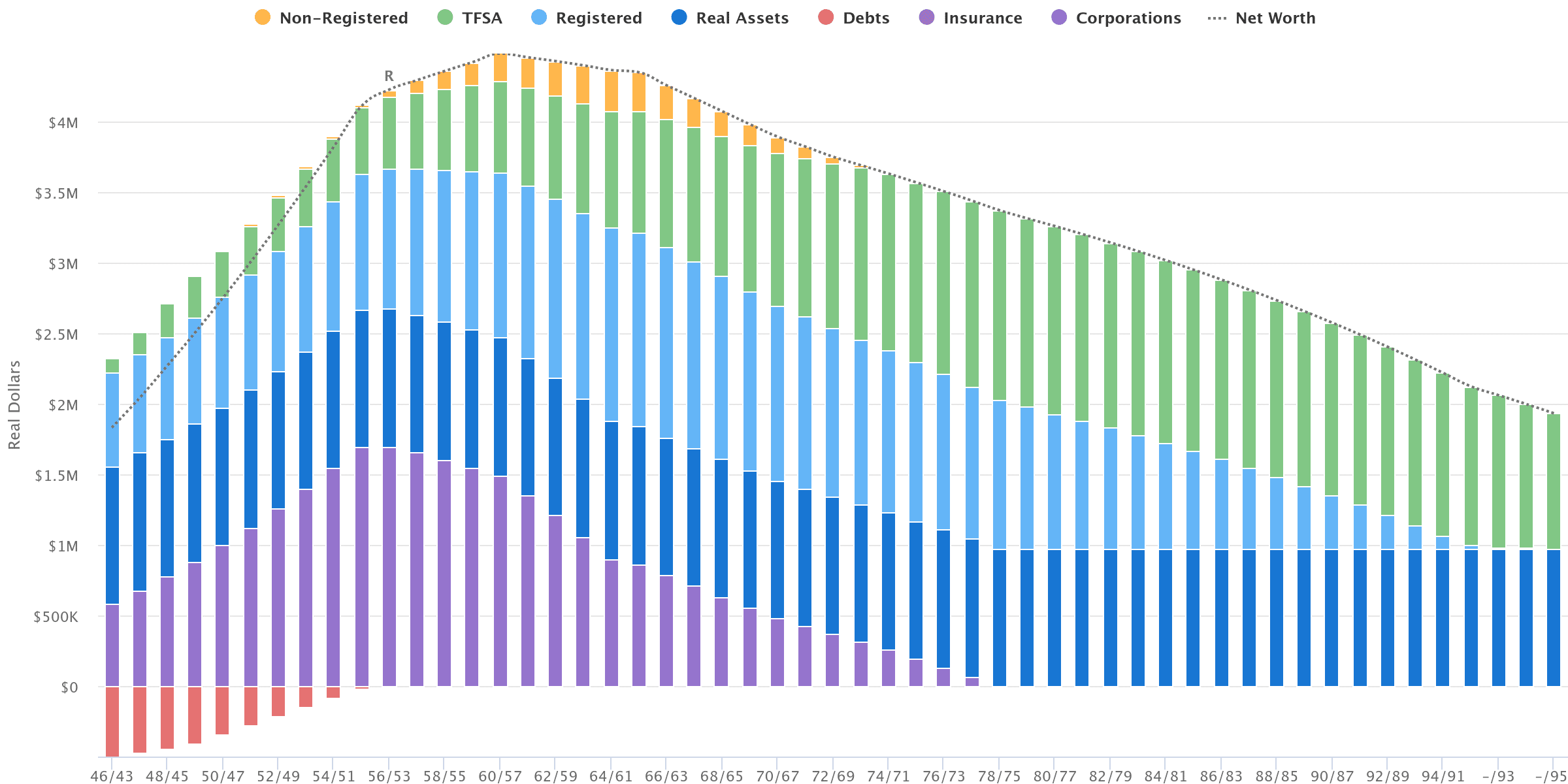

With that in mind, my idea is to stop working full-time in 10 years (55), work at 50% capacity for five years (60) and then at 25% capacity for five more years (65).

This gradual reduction in earnings while maintaining current spending means that the balance inside the corporation will start to decline as soon as age 56. Ideally, we’d exhaust our corporation before age 70 – but according to the chart shown above we’d still have corporate funds until 78.

That’s not as tax efficient as I’d like, but it’s a direct product of still working in some capacity until age 65. And I think my own sense of purpose and well-being is more important than having the most optimized and tax efficient retirement plan.

In summary: retire earlier if you want to optimize your tax efficiency.

I’d also convert my RRSP and LIRA to a RRIF and LIF at 65 to take advantage of pension income splitting. This means the amount of dividends we’d withdraw from the corporation will decrease to make room for the incoming RRIF and LIF income – allowing our average tax rates to remain smooth and consistent even as new puzzle pieces enter the fray.

CPP and OAS benefits will be moved out of the way (delayed to 70) to allow for these significant withdrawals, which is fine by me because I’ll take the enhanced and guaranteed income later in retirement.

Finally, there’s the TFSA. Unlike some people, we do not treat our TFSAs as an untouchable source of funds. Yes, it makes sense to keep our TFSAs intact as long as possible and take advantage of that tax free growth. But we also want to maximize our life enjoyment, and that will mean using the TFSA to top-up our spending once other income sources dry up.

We also need to consider one-time expenses that are more difficult to plan for such as vehicle replacement, home renovations or repairs, early financial gifts to kids, and bucket list type travel and experiences.

In my view, a TFSA is a great place to draw from to fund those one-time expenses in retirement as the withdrawal is tax-free, does not affect your OAS benefits, and you get the contribution room back the following year.

Final Thoughts on Retirement Income

My wife and I will go from receiving one income stream each in our working years to dealing with a combined 12 different income streams or sources in retirement.

- Corp (2)

- RRIF (2)

- LIF (1)

- CPP (2)

- OAS (2)

- Non-registered savings (1)

- TFSA (2)

Each of these puzzle pieces needs to be carefully placed to maximize growth, maximize income, and minimize taxes. And because life happens and goals change, nobody (and I mean nobody) is going to do this with absolute perfection.

But you can see why even the most financial literate person or the most sophisticated do-it-yourself investor might want to work with a financial planner to build a retirement plan, model out some scenarios to see what’s possible, and to stress-test their own ideas.

Clearly it’s not as straightforward as simply withdrawing 4% from your portfolio and adjusting for inflation. Which portfolio? We don’t have one bucket of money called retirement savings. You might have 8-12 different income sources to consider.

If you’re five years or less away from retirement, it’s worth reaching out to an advice-only planner to help fit all of your retirement income puzzle pieces together.